Blog-Details

05 Jun 2026

Buying a house requires a huge financial commitment from you. However, fire, severe storms, or sudden accidents can destroy your investment in just minutes. You need absolute certainty about your safety net before disaster strikes.

Many buyers grab a policy just because mortgage lenders demand it for the loan approval. Yet misunderstanding your policy leaves you exposed to unexpected expenses. Taking time to learn the basic details gives you tremendous confidence going forward.

Every property owner faces risks from nature and random accidents. Good homeowners insurance coverage shields your bank account from terrible loss. When an unexpected storm rips the roof off, your home insurance policy covers the cost, helping you avoid bankruptcy. Understanding the specific details prevents terrible surprises when you file a claim later.

You secure three main benefits when you buy a robust home insurance policy. It:

The main part of your policy defends the physical building. A sudden fire or windstorm causes severe property damage to walls and roofs. After such events, your home insurance carrier steps in to repair or rebuild the structure. You must choose adequate coverage limits to afford today’s expensive construction prices.

You should go for a policy that pays full replacement costs for the dwelling. This guarantees you can completely rebuild your home. Upgraded policies also pay extra money to meet modern building codes during reconstruction. Older houses often require completely new plumbing and electrical systems to meet modern safety rules.

Your policy protects much more than just the walls and the roof. Standard agreements include personal property coverage for the things inside a house. Furniture, electronics, and clothing cost thousands of dollars to replace after a disaster. A fire destroys everything inside the living room within a short time.

You must act smartly and create a thorough home inventory so that you can present it after a disaster. Taking videos of every single room provides excellent proof for the claims adjuster. This evidence forces home insurance companies to pay you faster and fairer. Without proof, you risk paying out of pocket to replace expensive items.

A major house fire forces you to move out for several months. Living elsewhere costs a lot of money for rent and food. Your policy should provide additional living expenses to handle these temporary relocation bills. This money pays for extended hotel stays while contractors finish the heavy reconstruction.

This relocation money pays for several daily necessities, like:

The home insurance provider writes checks for these bills after any covered loss makes the house unsafe.

Accidents happen frequently when guests visit your property for dinner or parties. Suppose that a friend slips on wet stairs and breaks a leg very badly. They can sue you for expensive hospital bills and lost work wages. Fortunately, personal liability coverage pays for their medical bills and your legal defense.

This protection literally saves you from losing everything you own in court. You need enough liability protection to match your total personal wealth value. If lawsuits exceed your policy maximums, courts can take your personal savings. You should always buy more liability protection than you think you actually need.

You must act quickly when a storm or fire damages your home. Follow these steps to ensure a smooth claims process:

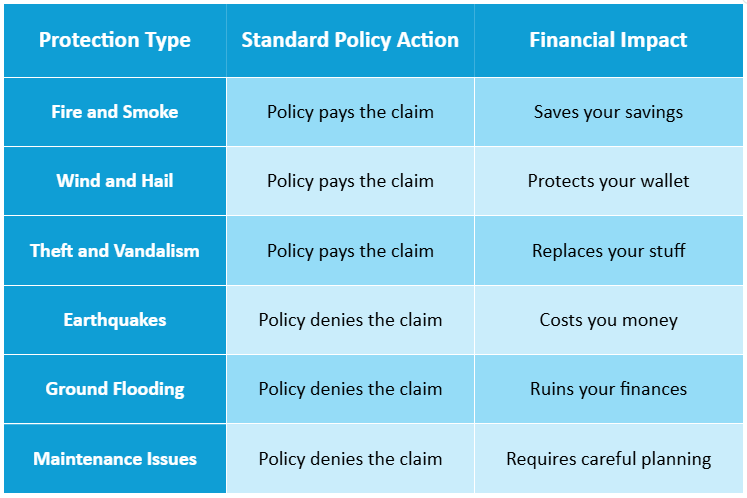

You can easily visualize the differences between standard inclusions and exclusions. Review this simple table to understand the boundaries of your policy.

Protecting your biggest asset demands expert guidance and a perfectly tailored plan. We understand the confusion surrounding complicated policy documents and strange industry terms.

Our team builds a strong defense wall around your specific daily life. Contact Warren Insurance Agency right now to secure your family. Let us handle the heavy lifting while you enjoy true peace of mind.

Standard policies completely exclude all damage from rising river waters and heavy rain floods. You must purchase a separate flood policy to secure this protection.

You should buy enough liability protection to match your total personal net worth exactly. This specific strategy effectively shields your savings accounts from aggressive lawsuit judgments.

Your carrier pays for temporary rent and food bills when major disasters destroy the house. This specific coverage keeps your daily life normal during heavy reconstruction.

Most standard policies pay to repair the terrible water damage from sudden pipe bursts. They usually refuse to pay the plumber for fixing the broken pipe.

Companies calculate your future risk based heavily on your past claims history. Filing multiple claims shows the carrier you present a much higher financial risk.

© 2026 Warren Insurance Agency. All Rights Reserved

Crafted with Love: DigiCorns